Investment Policy Statement

Introduction and Purpose

The intent of this Statement is to articulate an investment strategy with specific parameters that reflect the philosophy of the Board of Directors (the “Board’), thereby providing the Investment Committee (the “Committee”) with clearly defined policies and objectives. Although these policies and objectives are intended to govern investment activity, they are intended to be sufficiently flexible in order to be practical.

The Statement of Investment Policy was approved at a meeting of the Board of Directors on this July 16, 2014

Investment Philosophy Statement

- The following statements represent the investment principles and philosophy governing the investment of funds held by the Boise State University Foundation (the “Foundation”). These statements describe the core values and principles that form the basis for investment decision-making. These commonly held fundamental investment principles are: That the single most important decision that the Committee makes is the long-term asset allocation decision. As a result, nearly all of the absolute levels of investment returns are attributable to the Committee’s decisions regarding asset allocation, not manager implementation.

- That the capital markets are mean-reverting by nature. The Committee will therefore use longterm strategic asset class allocations and rebalance to those allocations within suitable ranges.

- That the achievement of long-term investment goals is derived directly from sound investment strategy decisions and efficient and consistent implementation of the strategy. Tactical asset allocation or manager allocation changes (usually in reaction to recent market performance) are likely to result in poor outcomes that will impair the long-term performance of the funds. As a result, the Committee will avoid tactical allocations to any manager or asset class in reaction to recent market conditions and instead rely on consistent portfolio rebalancing.

- That the achievement of the Foundation’s long-term investment goals necessitates that the investment strategy be based on using a combination of asset classes (and sub-asset classes) that has a reasonable probability of achieving the Foundation’s goals. As a result, the Committee will periodically conduct asset allocation studies to assess the probability of achieving its long-term goals.

- That market timing is ineffective as a market strategy for institutional funds. As a result, the Committee will remain fully invested in all long-term mandates and avoid interest rate anticipation as the primary means of adding value in fixed income mandates.

- That some asset classes are inefficient and active managers can clearly add value. Other asset classes, most notably the domestic large-cap equity market, are more efficient. As a result, the Committee may allocate assets between active and passive (index) allocations based on recommendations by the Consultant, utilizing active strategies only where there appears to be a clear benefit to doing so.

- That it is necessary to use long time frames and appropriate benchmarks to fairly evaluate active manager performance. Active managers are, by definition, different than a passive index. Differences in manager styles (growth, value) and market capitalization will have multi-year cycles. Additionally, active managers may be hired specifically to have different risk characteristics than popular indices. As a result, managers will have periods of both under- and out-performance relative to popular indices. In establishing individual manager investment objectives and in evaluating manager performance:

- The Consultant will use long time frames (rolling 3- and 5-year periods, or longer as appropriate),

- The Consultant will set appropriate investment objectives using relevant style and capitalization benchmarks,

- The Consultant will evaluate managers on a risk-adjusted basis.

- Investment implementation should be cost and resource effective. When evaluating new and current asset classes, managers and implementation strategies, the Consultant will evaluate both the implementation and monitoring costs and requirements, as well as the incremental benefits in terms of both risk and reward to the funds. The Consultant will utilize only those investment strategies that are expected to provide meaningful benefits to the funds, net of implementation and monitoring costs.

Delegation of Responsibilities

Relationship between Board and the Investment Committee

The Board is responsible for the overall stewardship of the Foundation. The Board has delegated to the Investment Committee the responsibility to oversee the Foundation’s investment activities on the Board’s behalf. The Committee will consist of an odd number of Directors with a minimum of seven. Appointment and terms of the Committee Chair and members are defined in the Foundation Bylaws. The members of the Investment Committee will be generally knowledgeable in investment and financial matters. The Committee may also have Advisors as specified in the Foundation’s Bylaws. The Committee has the responsibility to ensure that the assets of the Foundation are managed in a manner that is consistent with the policies and objectives ratified by the Board. In so doing, the Committee will comply with all applicable laws. The Committee members are required to discharge their duties solely in the interest of the Foundation and for the exclusive purpose of meeting the financial needs of the Foundation. The Committee is authorized to engage the services of a Consultant who possess the necessary specialized research capabilities and skills to meet the investment objectives and guidelines of the Foundation. The Committee will require the Consultant to adhere to any policies adopted by the Board. The Committee’s responsibilities include:

- Developing and recommending to the Board investment objectives that are consistent with the financial needs of the Foundation and the policy asset allocation consistent with meeting those objectives;

- Approving the selection of a Consultant.

- Reviewing and evaluating investment results in the context of predetermined performance standards and implementing corrective action as needed; and

- Recommending Spending Rate guidelines to the Board.

- Meeting with the Consultant at least quarterly to review and evaluate Consultant reports and provide feedback and direction to Consultant. Consultant reports will include overall investment performance and individual investment managers on a risk-adjusted basis after comparison to appropriate market indices or other benchmarks

- Investment manager and fund vehicle selection and retention decisions with recommendations provided by the Consultant

- Evaluating the performance of the Consultant at least annually prior to the annual contract renewal. Such evaluation will include the following criteria:

- Comparison of endowment portfolio performance to the goals set in the Return Need section of this Policy.

- Evaluation of Consulting and investment management fees. c. Evaluation of overall level of Consultant’s customer service (responsiveness; timeliness; accuracy; etc.).

- Review changes of Consultant ownership/management and investment philosophy.

- Other criteria determined by the Board and/or Committee

Consultant

The Committee will engage an independent investment consulting firm to assist the Committee’s activities. The Consultant is expected to be proactive in recommending changes in investment strategy, asset allocation and investment managers if the situation warrants change. The Consultant’s responsibilities include:

- Assisting in the development of investment policies, objectives and guidelines;

- Preparing asset allocation analyses as necessary and recommending asset allocation strategies with respect to the Foundation’s objectives;

- Researching and recommending Investment Managers and investment funds consistent with the Asset Allocation parameters defined in Appendix A.

- Preparing and presenting performance evaluation reports in accordance with CFA Institute promulgated standards;

- Attending Committee meetings to present evaluation reports no less than quarterly and at other meetings as requested;

- Reviewing contracts and fees for both current and proposed Investment Managers and Custodians;

- Providing research on specific issues and opportunities and assisting the Committee in special tasks;

- Proactive monitoring, advising and assisting with the endowment portfolio and rebalancing when outside target allocation ranges.

- Communicating investment policies and objectives to the Investment Managers, and monitoring their adherence to such policies and reporting all violations to the Committee and the Chief Operating Officer/Chief Investment Officer;

- Notifying the Committee and Foundation of any significant changes in personnel or ownership of the consulting firm;

- Notifying the Committee and Foundation of any significant changes in portfolio managers, personnel or ownership of any investment management firm hired by the Foundation;

- Notifying the Committee and Foundation of any litigation or commencement of a regulatory administrative proceeding or enforcement action in which any Investment Manager is involved;

- Providing recommendations with regards to proxy votes of mutual and commingled fund investments; and

- Overall, being proactive with the Administration of the Foundation and the Committee in the management of the Foundation investments.

Investment Managers

Investment Managers are expected, where applicable, to pursue their own investment strategies within the guidelines created for the manager in accordance with the Foundation’s asset allocation strategy and manager selection criteria. Coordination of the guidelines for the individual managers assures the combined efforts of the managers will be consistent with the overall investment objectives of the Foundation. The Committee may, where appropriate, choose to invest in pooled funds (mutual funds, commingled funds, and other forms of pooled investor capital) and recognizes that in the case of pooled fund investments that the relevant fund documents shall be the governing documents for the investment.

The Investment Managers’ responsibilities include:

- Investing assets under their management in accordance with agreed upon guidelines and restrictions;

- Exercising discretionary authority over the assets entrusted to them, subject to these guidelines and restrictions;

- Providing written documentation of portfolio activity, portfolio valuations, performance data and portfolio characteristics on a monthly basis in addition to other information as requested by the Committee, Foundation, or Consultant;

- Voting proxies for the assets under management (companies held within the portfolio) in the best interest of the Foundation;

- Annually providing to the Foundation either a copy of the investment advisor’s form ADV Part II (SEC required disclosure document), a copy of the investment company’s annual report, and/or a copy of the fund’s updated prospectus (SEC requirement at the end of the fiscal year).

- Notifying the Consultant, Committee and Foundation of any significant changes in portfolio management style, personnel or ownership of the investment management firm; and

- Notifying the Consultant, Committee and Foundation of any litigation or commencement of a regulatory administrative proceeding or enforcement action in which any Investment Manager is involved;

The Foundation Custodian’s responsibilities include:

- Providing timely reports detailing investment holdings and Foundation transactions monthly to the Foundation and Consultant.

- Providing an annual summary report to the Foundation and the Consultant within 30 days following each fiscal year end. The report will include the following:

- Statement of all property on hand;

- Statement of all property received representing contributions to the Foundation;

- Statement of all sales, redemptions and principal payments;

- Statement of all distribution from and contributions to the Foundation;

- Statement of all expenses paid;

- Statement of all purchases; and

- Statement of all income.

- Providing all normal custodial functions including security safekeeping, collection of income, settlement of trades, collection of proceeds of maturing securities, daily investment of cash, etc.

- Preparing additional Foundation reports as requested by the Board, Committee, Consultant, or Executive Director.

Investment Policies and Objectives

Endowed Fund Objectives and Guidelines

Objective: The Investment objective is to provide a rate of return over inflation sufficient to support in perpetuity the mission of the Foundation. It is particularly important to preserve the value of the assets in real terms to enable the Foundation to maintain the purchasing power of the spending on programs and administration without eroding the real value of the principal corpus of the Foundation.

General Investment Considerations and Constraints:

- Risk: The Committee will seek to limit the overall level of risk commensurate with the chosen Policy Asset Allocation.

- Liquidity: At times, cash may be required to satisfy the needs of the Foundation. The Foundation should have sufficient liquid assets to meet such foreseeable requirements.

- Time Horizon: The Foundation has an infinite life. An investment Time Horizon of twenty years is appropriate.

- Taxes: The Foundation is tax-exempt.

Return Need

The long-term investment return should be sufficient to cover the Spending Rate, Administrative Fee and the expected rate of inflation. The Spending Rate is currently 4% and the Administrative Fee is 1.5%, so the Foundation’s real return need net of inflation is 5.5%. There may be periods of time where the Consultant’s projections for future returns do not support the stated return need without assuming an undiversified portfolio strategy that would introduce imprudent levels of risk. It shall be the philosophy of the Committee to maintain a diversified long-term strategy during such periods, and to also consider to the extent possible elements of the spending rate and administrative fee that can be reasonably adjusted over time to better support the perpetual mission of the Foundation. The following goals are designed to support achievement of the Foundation’s Investment Objective and are net of (after) investment expenses.

- Total Foundation assets should achieve an annualized rate of return equal to or greater than that of the Long-Term Return Need over a full market cycle.

- Total Foundation assets should return, over a full market cycle, a nominal rate of return greater than or equal to a hypothetical index portfolio consisting of 32% Russell 3000, 33% MSCI All Country World ex-US, 25% Barclays Aggregate Bond, 3% Barclays U.S. TIPS, 2% S&P Global REIT Index, 2% S&P Global Natural Resources Index, and 3% S&P MLP Index (TR).

Spending Rate Policy

Spending Rate

The Spending Rate of the Foundation will be reviewed by the Committee periodically in light of evolving trends with respect to investment performance and the needs of the Foundation and will be adjusted as necessary.

As allowed by the Uniform Prudent Management of Institutional Funds Act adopted by the state of Idaho in July 2007, the Foundation may spend at its Spending Rate from “underwater” funds for the purpose of the specific fund. An underwater fund is defined as one in which the market balance is below the sum of the gifts contributed to the fund (“historical gift value”).

Unless otherwise directed by the donor for a specific endowed gift, the annual Spending Rate shall not exceed 4% of the trailing 3-year average market value of the endowment, as determined each December 31st. The Spending Rate shall be reduced from 4% to 2% when the market value is below 90% of the historical gift value.

In the event the spending rate is reduced from 4% to 2% donors may be asked to consider new gifts to keep their endowment distributions at the 4% level and the Foundation Board may consider funding from unrestricted funds. In the event the Foundation Board approves the use of unrestricted funds when endowment distributions are reduced, a special distribution from the endowment to refund the Foundation may be considered once the market value of the endowment is sufficiently above the historical gift value.

Total Return Policy

The Board has adopted a “total return” approach to calculating investment returns. In recognition of these facts, the Committee will consider the endowments’ total return from both income and net realized and unrealized capital gains when recommending the Spending Rate Policy. When distributions are made, they will be withdrawn from the endowment regardless of the portion of the total return that is from capital gains or from income, subject to applicable gift agreement restrictions.

Administrative Fee

An Administrative Fee of 1.5% of the market value of the endowment will be calculated and distributed monthly on a pro-rata basis. The Administrative Fee will be reviewed and evaluated annually as part of the preparation of the Foundation’s annual budget. Efforts will be made to gradually reduce the administrative fee percentage as the endowment grows.

Asset Allocation

The single most important decision made by the Committee is the Policy Asset Allocation decision. Investment research has determined that a significant portion of a portfolio’s investment behavior can be attributed to: (1) the asset classes/styles which are employed by the Foundation; and (2) the weighting of each asset class/style.

It is the responsibility of the Committee to identify the Policy Asset Allocation that offers the highest probability of achieving the Foundation’s Investment Objectives. The Committee, with guidance and recommendations from their Consultant, shall review the asset mix on an ongoing basis and recommend revisions as necessary.

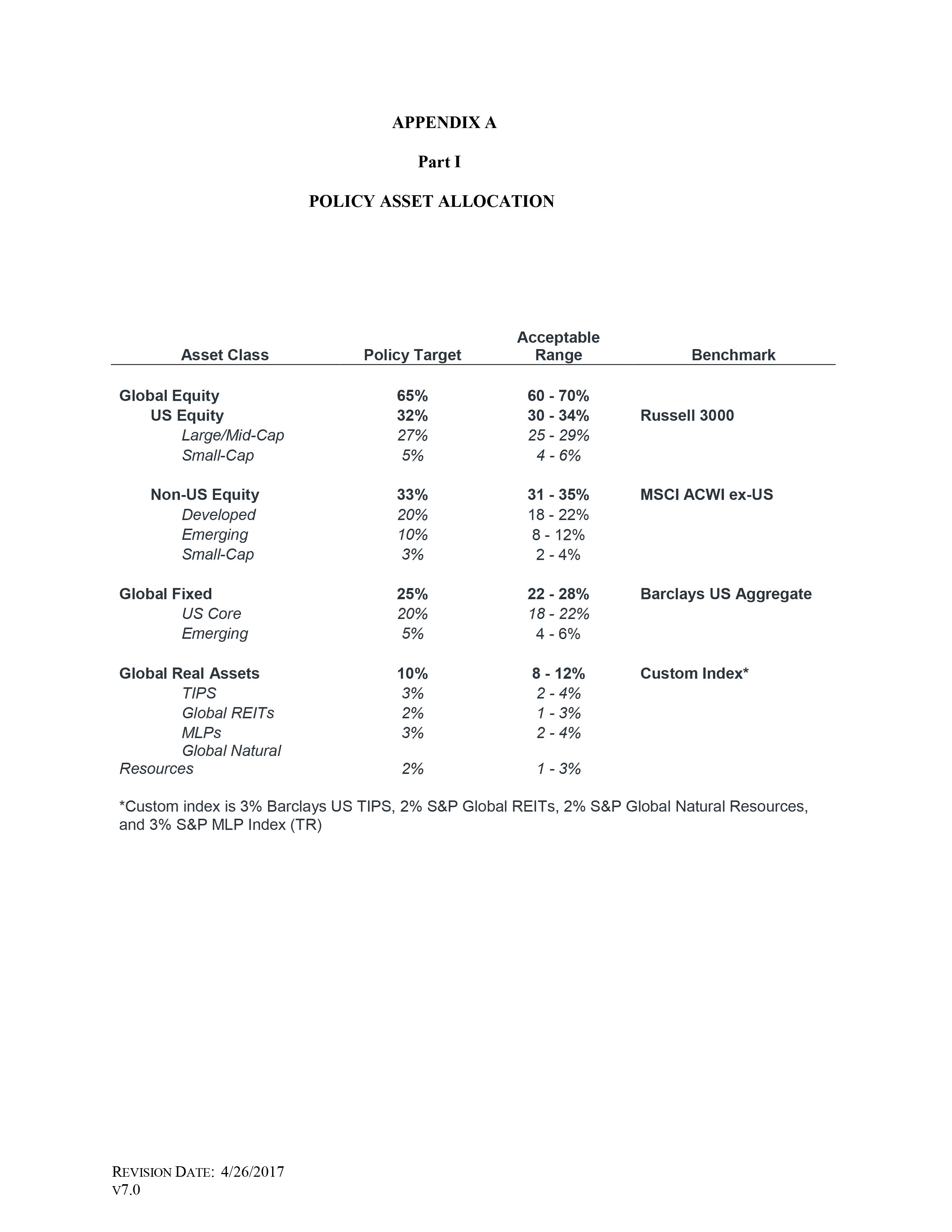

The Policy Asset Allocation shall be determined based on a comprehensive asset allocation study completed by the Consultant and reviewed from time to time by the Committee. The Policy Asset Allocation of the Foundation, as presented in Appendix A, is designed to give balance to the overall structure of the Foundation’s investment program over the Time Horizon. However, many factors over time may necessitate an asset allocation review and possible rebalancing.

Some of these factors include:

- The Investment Committee’s assessment of the intermediate or long term outlook for different types of asset classes and styles;

- The consultant’s assessment of the intermediate or long term outlook for different types of asset classes and styles; and

- Divergence in the performance of the different asset classes and styles.

Permissible Investments

The Policy Asset Allocation of the Foundation is expected to include a wide range of asset classes. These asset classes and their relative comparative indices are displayed below.

Comparative Indices for Investment Managers

Asset Class (Comparative Index)

Global Equity

- US Large Cap (S&P 500)

- US Mid Camp (CRSP S Mid Cap)

- US Small Cap (Russell 2000)

- US Micro Cap (Russel Micro Cap)

International Equity

- Non-US Large/Mid-Cap Developed (MSCI EAFE)

- Non-US Small Cap (MSCA EAFE Small Cap)

- Emerging Markets (MSCI Emerging Markets)

- Global Fixed Income

- Core (Barclays US Aggregate)

- Emerging Markets (JP Moran EMBI Global Diversified)

Global Real Assets

- TIPS (Barclays US Tips)

- Global REITs (S&P Global REIT)

- Global Natural Resources (S&P Global Natural Resources)

- Master Limited Partnerships – MLPs (S&P MLP Index – TR)

Portfolio Rebalancing

Since asset allocation is the most critical component of the Foundation’s returns, it is desirable to rebalance the portfolio periodically to minimize deviations from the Policy Asset Allocation mix.

The Consultant shall be responsible for coordinating rebalancing of the portfolio with Foundation Staff in the event any individual marketable asset class differs from the allowable Policy ranges (minimum or maximum). See Appendix A for the Policy Target allocation and allowable ranges.

The staff will inform the Committee whenever rebalancing takes place.

Other Non-Endowment Assets

The Board may, from time to time, establish investment portfolios other than the Endowment Fund. Asset allocation and investment guidelines for these portfolios will be developed as needed and, when appropriate, in consultation with the donor. The Foundation Investment Objectives and Guidelines for restricted funds are stated in Appendix B to this Policy Statement. The Foundation Investment Objectives and Guidelines for assets from life income agreements (charitable remainder trusts and charitable gift annuities) are stated in Appendix C to this Policy Statement.

The Foundation Investment Objectives and Guidelines for unrestricted assets are stated in Appendix D to this Policy Statement.

The Foundation owns several parcels of real estate as the result of individual gifts and purchases made in the interest of the University. The Investment Committee has appointed a real estate subcommittee to monitor these properties, review potential gifts and make recommendations regarding disposition to the Board.

The trust assets and parcels of real estate are not included in the Foundation’s investment asset allocation, nor are they included in the Consultant’s purview.

Investment Policies for Investment Managers

The following are performance goals and constraint guidelines placed on individual managers within specific asset classes:

All Traditional Managers

- Index (passive) managers shall be terminated if performance or volatility significantly differs from that of the benchmark.

- Active managers may be terminated due to philosophical changes, management turnover, poor long-term investment performance or other material changes.

Alternative Investments

Alternative investment managers typically must have significant latitude in the strategies and investments they make and the leverage they introduce into a portfolio. As a result, it is generally not feasible to impose guidelines and restrictions on such managers. Instead, the Committee may choose to terminate a manager, subject to the manager’s liquidation policy, if they are dissatisfied with the manager and/or his strategy.

Other

- Securities Lending: Investment Managers (via a written contract with the Foundation), may engage in securities lending, or the “loan” of the Foundation’s securities in return for interest, to broker dealers as a means of enhancing income.

- Related Party Transaction: The Foundation will not loan funds to related parties, defined as an officer, Board member, Committee member, employee, or donor, either current or prospective.

Procedure for Revising the Statement of Investment Policy

This Statement of Investment Policy will be reviewed at least annually by the Committee. The Board must approve material changes to the Statement. Any deviation from the Policy Asset Allocation of the combined asset sectors (i.e., total equities, total fixed income, or total real assets) would represent a material change and shall be approved by the Board.

Conflicts of Interest

All persons responsible for investment decisions or who are involved in the management of the Foundation or who are consulting to, or providing any advice whatsoever to the Committee, shall comply with the Foundation’s Conflict of Interest Policy.

Any members of the Committee responsible for investment decisions or who are involved in the management of the Foundation shall refuse any remuneration, commission, gift, favor, service or benefit that might reasonably tend to influence them in the discharge of their duties, except as disclosed in writing to and agreed upon in writing by the Committee. The intent of this provision is to eliminate conflicts of interest between committee membership and the Foundation. Failure to disclose any material benefit shall be grounds for immediate removal from the committee. This provision shall not preclude the payment of ordinary fees and expenses to the Foundation’s custodian(s), Investment Managers, or Consultant in the course of their services on behalf of the Foundation.

Appendix A Part 1: Policy Asset Allocation

{kind=link}

Appendix B: Restricted Funds (Investment Objectives and Guidelines)

Objectives and Guidelines

Objective: The Investment objective is to provide for the short-term cash flow needs of the Foundation. General Investment

Considerations and Constraints:

- Risk: The Committee will seek to limit the overall level of risk commensurate with the chosen Policy Asset Allocation. Safety of principal is particularly important.

- Liquidity: The investment in individual securities for which the benchmark is the BofA Merrill Lynch 3 month Treasury Bill Index serves as a cash surrogate, therefore, the investment strategy should have sufficient liquidity to meet foreseeable requirements.

- Time Horizon: Although the Foundation has an infinite life, the Time Horizon for investment of most these funds is five years, however a portion of the funds may be invested in a longer-term strategy based on an analysis of the actual cash flow.

- Taxes: The Foundation is tax-exempt.

Investment Managers

Investment Managers are expected to pursue their own investment strategies within the guidelines created for the manager in accordance with the Foundation’s asset allocation strategy and manager selection criteria. Coordination of the guidelines for the individual managers assures the combined efforts of the managers will be consistent with the overall investment objectives of the Foundation.

Investment Managers in the Fund are held to the same requirements as delineated in the “Delegation of Responsibilities” section of the Foundation’s IPS.

Return Need

Non-endowed Foundation assets should achieve an annualized rate of return which meets the General Investment Considerations and Constraints above.

Asset Allocation

The single most important decision made by the Committee is the Policy Asset Allocation decision. Investment research has determined that a significant portion of a portfolio’s investment behavior can be attributed to: (1) the asset classes/styles which are employed by the Foundation; and (2) the weighting of each asset class/style.

It is the responsibility of the Committee to identify the Policy Asset Allocation that is consistent with achieving the Foundation’s Investment Objectives. The Committee, with guidance and recommendations from their Consultant, shall review the asset mix on an ongoing basis and recommend revisions as necessary.

The Policy Asset Allocation shall be determined based on a comprehensive cash flow analysis by the Administration and asset allocation study by the Consultant and reviewed from time to time by the Committee. The Policy Asset Allocation of the Foundation is designed to give balance to the overall structure of the Foundation’s investment program over the Time Horizon. However, many factors over time may necessitate an asset allocation review and possible rebalancing. These factors include an ongoing assessment by the Administration, Consultant and the Committee of the comparative long-term outlook for all available types of asset classes and styles.

Permissible Investments

The Policy Asset Allocation of the Foundation is expected to be in asset classes which are consistent with the comparative indices below:

- Individual securities for which the benchmark is Bof A Merrill Lynch 3-month Treasury Bill Index.

- Individual securities for which the benchmark is BofA Merrill Lynch 1-3 year Index.

- Individual securities for which the benchmark is BofA Merrill Lynch 3-5 year Index

- The balances in these strategies will change over time due to investment gains and losses. • Funds will be invested so that maturities match expected outflows.

- Up to $5MM in restricted funds may be invested in the Endowment Strategy.

Individual Debt Security Guidelines

- Money market instruments must be rated A-2/P-2 or better at time of purchase.

- In the event of an instrument downgrade, the Manager shall notify the Committee and provide an evaluation and recommended course of action.

Procedure for Revising Guidelines

The investment policy and performance goals will be reviewed annually or when deemed necessary by the Committee. The Board must approve material changes to the Investment Objectives and Guidelines for non-endowed Foundation funds.

Appendix C: Investment of Assets from Life Income Agreements

Life Income Agreement Definition

A life income agreement is a split interest agreement between the Foundation and a donor which provides regular payments for the life of the beneficiary(ies) or for a set term of years. Examples are Charitable Remainder Trusts (CRTs) and Charitable Gift Annuities (CGAs). Refer to the Life Income Agreement Policy for definitions of each type of life income agreement.

Objectives and Guidelines

Objective: Life income assets are invested to meet the goals of the donor and Foundation using varying investment strategies based on the uniqueness of each life income agreement.

Guidelines: The Foundation’s Investment Committee will have the responsibility and authority for determining the most appropriate investment strategies and vehicles for all life income agreements.

Charitable Remainder Trust

- Because each CRT will have different objectives, the Investment Committee shall set an investment strategy for each based on collected data and the terms delineated in the CRT document. CRTs may or may not be co-mingled with other assets of the Foundation.

- The Investment Committee will determine the investment strategy for each CRT for which the Foundation is the trustee.

Charitable Gift Annuities

- The Foundation will maintain CGAs in an investment pool that may be separate from its general investment pool.

- The full market value of the contributed assets will be admitted to the CGA investment pool and will be maintained for the life of the last remaining annuitant.

- All CGAs will share their fair portion of investment management fees.

- The assets of each CGA shall be invested approximately as follows:

- 50% in equities;

- 50% in fixed income vehicles such as bonds;

Reporting

Foundation staff will report investment results, portfolio mix, and growth in the life income agreement program to the Investment Committee at least annually.

Procedure for Revising Guidelines

The investment policy and performance goals will be reviewed annually or when deemed necessary by the Committee. The Board must approve material changes to the Investment Objectives and Guidelines for life income agreement funds.